Executive Summary

- The Coronavirus is forcing individuals, corporations, schools, hospitals and governments to adapt to sudden changes.

- The Federal Reserve has signaled its commitment to support the economic recovery for an extended period and has introduced a new policy framework of targeting average inflation of 2% over time.

- The CARES act has provided a significant amount of fiscal stimulus and investors remain keenly interested in the potential for additional fiscal stimulus measures.

- Excepting a few industries that almost can’t operate amidst a pandemic, earnings have been “less bad” than anticipated.

- The upcoming election is top of mind for many investors and emotions are running high.

- We note that historically, the market has performed well most of the time with little discernable difference between Democrat and Republican administrations, higher taxes and lower taxes, more regulation and less regulation and all the surprises that history has brought.

- Risk control and thorough planning remain critical to achieving financial goals.

Well….at least there’s football. The country and the world have been turned upside down by the Coronavirus, an unforeseen wrecking ball that has taken over 1 million lives globally; caused millions of job losses; and isolated everyone. The words “new normal” have been used to describe the world in which we now live. I don’t think it fits. I believe it is the world of the audible: changing the play at the line of scrimmage based on field conditions. The Federal Reserve (the Fed) has called multiple audibles: 0% fed funds rate, reinstituting quantitative easing (bond purchases) and reapportioning its dual mandate favoring full employment. The United States government has called an audible with enormous fiscal stimulus in response to Coronavirus displacement. Families and businesses are calling audibles every day to make ends meet, care for children and protect themselves without giving up on a little enjoyment along the way. Peyton Manning made the word “Omaha!” famous. He said it a lot, he said it loud and nobody knew what he was talking about. Obviously, he was looking at the defense and what they might throw at him. What does it mean? During his career he answered the question with sarcasm and misdirection. Now that he has retired, he’s come clean. “Omaha!” means the play has changed. I think “Omaha!” is a more relevant description of the current times than “the new normal.” We are resourceful and determined creatures. We’re just trying to find our way.

The Fed has followed an aggressive response to the Coronavirus induced shutdowns with a significant rethinking of the approach to inflation targeting. On August 27, 2020, the Fed released its statement on Longer-Run Goals and Monetary Policy Strategy in response to a large-scale evaluation of the effectiveness of Fed policy. In effect, the statement seems to rebalance priorities with greater emphasis on a broader conception of full-employment and greater flexibility around the target interest rate. Instead of targeting 2% inflation, the new strategy is to target an average of 2% inflation over time. The statement represents yet another firm commitment by the Fed to support economic recovery with a willingness to overshoot the 2% inflation target for an unspecified period in order to achieve durable gains in employment.

The Federal government has failed to follow-up the $2.2 trillion Coronavirus Aid, Relief, and Economic Security (CARES) act with another round of stimulus due to differences over the size and scope of the relief. The specific and generous income replacement provided by the CARES act lapsed at the end of July. Progress or reversals on a deal among lawmakers seems to determine the direction of the equity markets these days.

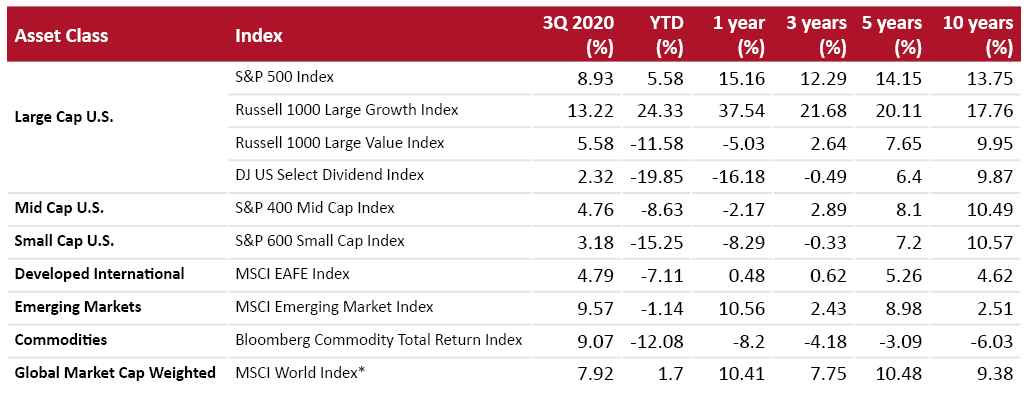

Despite a decline for September, the S&P 500 returned 8.93% for the 3rd quarter. The index currently sits about 4% below the September 2 all-time high and is up 5.84% year-to-date. The recovery is the fastest on record from bear market levels. The speed and intensity of the recovery against a less than all clear backdrop has many concerned. At the most basic level, companies have adapted. Excepting a few industries that almost can’t operate amidst a pandemic, earnings have been “less bad” than anticipated. According to FactSet Research’s StreetAccount, the blended second quarter earnings decline for the S&P 500 was -31.8% as of August 28, 2020 on a revenue decline of -8.7%. Expectations were much worse. In fact, 84% of reporting companies beat expectations. Of those that beat, the average reported earnings per share was 23% better than anticipated. The quarter included most of the lockdown period. While the results are not impressive, they probably do represent a bottom assuming that new lockdowns are not imposed. The averages reflect outcomes ranging from accelerated growth to painful and unsustainable cost cutting in order to remain viable.

Equity Market Index Returns

As of September 30, 2020

*The U.S. represents about 51% of the MSCI World Index.

All returns greater than one year are annualized. Source: Greenhill Market Index Review as of September 30, 2020

Rising stock prices and declining earnings can only mean rising multiples. The S&P 500 is trading for 22.1x next-twelve months earnings estimates, a premium to the 25-year average of around 16x. Estimates forecast a quick recovery. The current consensus of estimates represents an 18% 2020 decline from 2019 followed by 25% increase in 2021. Despite the pain and displacement Coronavirus has caused, it is our belief that the market is not predicting a “new normal” at all. Rather, it is predicting that low rates, ingenuity and time will restore a normal economy. In other words, the speed of the recovery reflects the belief that the recession is event driven rather than structural and that we have the wherewithal to overcome the “event.” Despite somewhat lofty valuations for the broad equity market, the S&P’s rebound has been dominated by handful of very large Technology companies who have benefitted from the acceleration of well-known structural business trends. Looking beyond Large Cap Technology, there remain areas of the market that indicate better relative value opportunities. Many of these areas would be cyclical beneficiaries of continued progress against the Coronavirus.

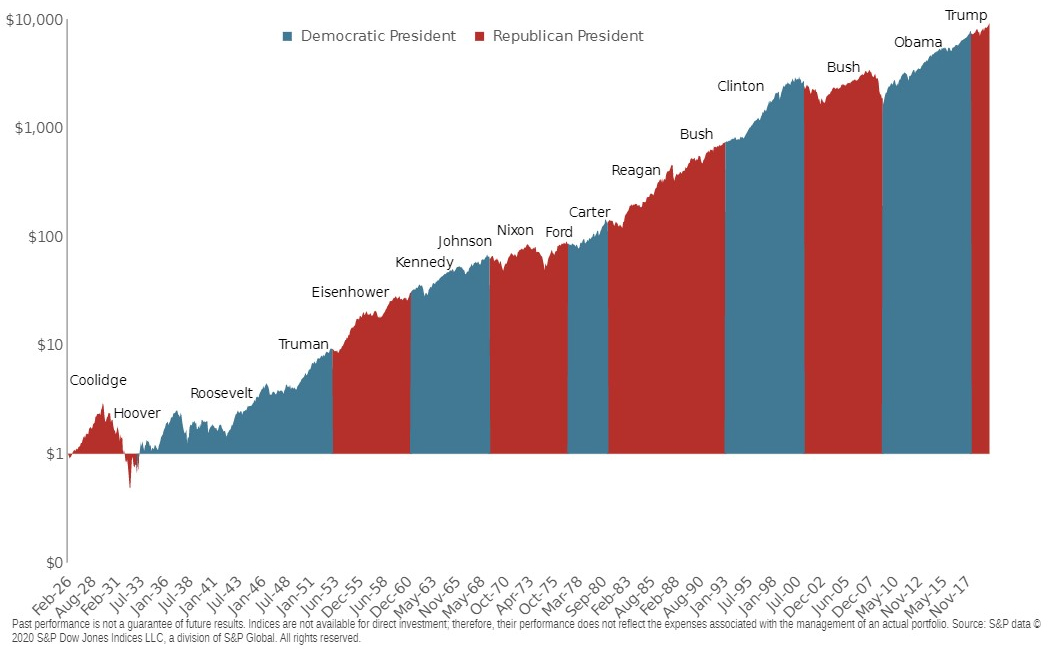

While the market seems unified in the belief that Coronavirus is less of a problem than initially forecast and the full recovery will come within the foreseeable future, the electorate is not. The November 3 election is on everyone’s mind. As a rule, politics and investing do not mix well. The market has performed well most of the time with little discernable difference between Democrat and Republican administrations, higher taxes and lower taxes, more regulation and less regulation and all the surprises that history has brought. That said, emotions run high at election time and the two parties offer very different policy alternatives for Coronavirus, foreign policy, healthcare, wealth disparity and pretty much everything else. The idiosyncratic concern with this election is the possibility of a contested election result due to modified voting procedures for Coronavirus, specific statements and how close the last presidential election was. We don’t know how to handicap this risk. At some point, you just have to trust in our institutions and assume that we can work through it if there is a contest. As in sales, a quick decision for the other guy is probably the second-best option for most voters/ investors.

Markets Have Rewarded Long-Term Investors under a Variety of Presidents

Growth of a Dollar Invested in the S&P 500: January 1926 - December 2019

Source: https://awealthofcommonsense.com/2020/10/dont-mix-your-politics-with-your-portfolio/

The Fed’s actions and persistently low inflation have confounded the conventional wisdom that a risk averse investor had options. Bond yields have fallen to the point where any significant allocation reduces expected return to the point at which all but the wealthiest of investors must maintain a higher allocation to risk assets than traditionally believed to meet goals. Many find this disturbing and we sympathize. Every traditional rule of thumb recommended reducing allocations to risk assets and adding fixed income as the reliability of that income stream became more important (ie retirement). Today, a traditional balanced allocation offers significantly less income than expected and creates a similar drag on total return as cash. The alternatives are to increase equity allocation, accept lower yields and moderate the plan or seek alternatives for the fixed income component. We strongly advise against the final alternative. “Reaching for yield” has a long and painful history. We believe that the enablers of higher than market yield create risks that are often obscured: leverage, credit, fraud. There is no free lunch and we believe that investors should only take risks for which they are compensated. Our advice is to prepare for higher than normal cash balances as bonds mature and equities are rebalanced to control risk. Evidence of growth should steepen the yield curve over time, restoring an acceptable alternative for long-term investment. In the meantime, risk control and thorough planning remain critical to achieving financial goals.

The economy saw a quick snap back after the 31.4% second quarter GDP decline, but seems to have plateaued following the run-off of enhanced unemployment benefits. The unemployment rate fell from 14.7% in April to 7.9% in October reflecting furloughed employees going back to work, growth in certain industries and a reduction in the labor force. Weekly initial unemployment claims have stabilized at a little under 900,000 after an initial spike. Prior to the pandemic, the average was around 200,000. Industrial surveys have moved back above 50, which marks projected future growth. We were in a bit of an industrial lull prior to the pandemic, so inventory and order backlogs did not represent the headwinds that they otherwise might have. While things are “less bad,” they aren’t good. Hospitality, airlines and countless small and large businesses that support them are in crisis until people are comfortable venturing out again.

The world is uncertain in the face of Coronavirus. So uncertain, that a market that typically hates uncertainty seems to be ignoring it. Coronavirus is showing us a lot of different looks and forcing individuals, corporations, schools, hospitals and governments to make changes at the line of scrimmage to adapt to sudden changes. The equity markets are telling us that we will get through this, but it doesn’t feel great out there. We’ll elect a president in less than a month. We don’t know the escape velocity from the pandemic because it relies on unpredictable human behavior. “Omaha!”

Executive Summary

Well….at least there’s football. The country and the world have been turned upside down by the Coronavirus, an unforeseen wrecking ball that has taken over 1 million lives globally; caused millions of job losses; and isolated everyone. The words “new normal” have been used to describe the world in which we now live. I don’t think it fits. I believe it is the world of the audible: changing the play at the line of scrimmage based on field conditions. The Federal Reserve (the Fed) has called multiple audibles: 0% fed funds rate, reinstituting quantitative easing (bond purchases) and reapportioning its dual mandate favoring full employment. The United States government has called an audible with enormous fiscal stimulus in response to Coronavirus displacement. Families and businesses are calling audibles every day to make ends meet, care for children and protect themselves without giving up on a little enjoyment along the way. Peyton Manning made the word “Omaha!” famous. He said it a lot, he said it loud and nobody knew what he was talking about. Obviously, he was looking at the defense and what they might throw at him. What does it mean? During his career he answered the question with sarcasm and misdirection. Now that he has retired, he’s come clean. “Omaha!” means the play has changed. I think “Omaha!” is a more relevant description of the current times than “the new normal.” We are resourceful and determined creatures. We’re just trying to find our way.

The Fed has followed an aggressive response to the Coronavirus induced shutdowns with a significant rethinking of the approach to inflation targeting. On August 27, 2020, the Fed released its statement on Longer-Run Goals and Monetary Policy Strategy in response to a large-scale evaluation of the effectiveness of Fed policy. In effect, the statement seems to rebalance priorities with greater emphasis on a broader conception of full-employment and greater flexibility around the target interest rate. Instead of targeting 2% inflation, the new strategy is to target an average of 2% inflation over time. The statement represents yet another firm commitment by the Fed to support economic recovery with a willingness to overshoot the 2% inflation target for an unspecified period in order to achieve durable gains in employment.

The Federal government has failed to follow-up the $2.2 trillion Coronavirus Aid, Relief, and Economic Security (CARES) act with another round of stimulus due to differences over the size and scope of the relief. The specific and generous income replacement provided by the CARES act lapsed at the end of July. Progress or reversals on a deal among lawmakers seems to determine the direction of the equity markets these days.

Despite a decline for September, the S&P 500 returned 8.93% for the 3rd quarter. The index currently sits about 4% below the September 2 all-time high and is up 5.84% year-to-date. The recovery is the fastest on record from bear market levels. The speed and intensity of the recovery against a less than all clear backdrop has many concerned. At the most basic level, companies have adapted. Excepting a few industries that almost can’t operate amidst a pandemic, earnings have been “less bad” than anticipated. According to FactSet Research’s StreetAccount, the blended second quarter earnings decline for the S&P 500 was -31.8% as of August 28, 2020 on a revenue decline of -8.7%. Expectations were much worse. In fact, 84% of reporting companies beat expectations. Of those that beat, the average reported earnings per share was 23% better than anticipated. The quarter included most of the lockdown period. While the results are not impressive, they probably do represent a bottom assuming that new lockdowns are not imposed. The averages reflect outcomes ranging from accelerated growth to painful and unsustainable cost cutting in order to remain viable.

Equity Market Index Returns

As of September 30, 2020

*The U.S. represents about 51% of the MSCI World Index.

All returns greater than one year are annualized. Source: Greenhill Market Index Review as of September 30, 2020

Rising stock prices and declining earnings can only mean rising multiples. The S&P 500 is trading for 22.1x next-twelve months earnings estimates, a premium to the 25-year average of around 16x. Estimates forecast a quick recovery. The current consensus of estimates represents an 18% 2020 decline from 2019 followed by 25% increase in 2021. Despite the pain and displacement Coronavirus has caused, it is our belief that the market is not predicting a “new normal” at all. Rather, it is predicting that low rates, ingenuity and time will restore a normal economy. In other words, the speed of the recovery reflects the belief that the recession is event driven rather than structural and that we have the wherewithal to overcome the “event.” Despite somewhat lofty valuations for the broad equity market, the S&P’s rebound has been dominated by handful of very large Technology companies who have benefitted from the acceleration of well-known structural business trends. Looking beyond Large Cap Technology, there remain areas of the market that indicate better relative value opportunities. Many of these areas would be cyclical beneficiaries of continued progress against the Coronavirus.

While the market seems unified in the belief that Coronavirus is less of a problem than initially forecast and the full recovery will come within the foreseeable future, the electorate is not. The November 3 election is on everyone’s mind. As a rule, politics and investing do not mix well. The market has performed well most of the time with little discernable difference between Democrat and Republican administrations, higher taxes and lower taxes, more regulation and less regulation and all the surprises that history has brought. That said, emotions run high at election time and the two parties offer very different policy alternatives for Coronavirus, foreign policy, healthcare, wealth disparity and pretty much everything else. The idiosyncratic concern with this election is the possibility of a contested election result due to modified voting procedures for Coronavirus, specific statements and how close the last presidential election was. We don’t know how to handicap this risk. At some point, you just have to trust in our institutions and assume that we can work through it if there is a contest. As in sales, a quick decision for the other guy is probably the second-best option for most voters/ investors.

Markets Have Rewarded Long-Term Investors under a Variety of Presidents

Growth of a Dollar Invested in the S&P 500: January 1926 - December 2019

Source: https://awealthofcommonsense.com/2020/10/dont-mix-your-politics-with-your-portfolio/

The Fed’s actions and persistently low inflation have confounded the conventional wisdom that a risk averse investor had options. Bond yields have fallen to the point where any significant allocation reduces expected return to the point at which all but the wealthiest of investors must maintain a higher allocation to risk assets than traditionally believed to meet goals. Many find this disturbing and we sympathize. Every traditional rule of thumb recommended reducing allocations to risk assets and adding fixed income as the reliability of that income stream became more important (ie retirement). Today, a traditional balanced allocation offers significantly less income than expected and creates a similar drag on total return as cash. The alternatives are to increase equity allocation, accept lower yields and moderate the plan or seek alternatives for the fixed income component. We strongly advise against the final alternative. “Reaching for yield” has a long and painful history. We believe that the enablers of higher than market yield create risks that are often obscured: leverage, credit, fraud. There is no free lunch and we believe that investors should only take risks for which they are compensated. Our advice is to prepare for higher than normal cash balances as bonds mature and equities are rebalanced to control risk. Evidence of growth should steepen the yield curve over time, restoring an acceptable alternative for long-term investment. In the meantime, risk control and thorough planning remain critical to achieving financial goals.

The economy saw a quick snap back after the 31.4% second quarter GDP decline, but seems to have plateaued following the run-off of enhanced unemployment benefits. The unemployment rate fell from 14.7% in April to 7.9% in October reflecting furloughed employees going back to work, growth in certain industries and a reduction in the labor force. Weekly initial unemployment claims have stabilized at a little under 900,000 after an initial spike. Prior to the pandemic, the average was around 200,000. Industrial surveys have moved back above 50, which marks projected future growth. We were in a bit of an industrial lull prior to the pandemic, so inventory and order backlogs did not represent the headwinds that they otherwise might have. While things are “less bad,” they aren’t good. Hospitality, airlines and countless small and large businesses that support them are in crisis until people are comfortable venturing out again.

The world is uncertain in the face of Coronavirus. So uncertain, that a market that typically hates uncertainty seems to be ignoring it. Coronavirus is showing us a lot of different looks and forcing individuals, corporations, schools, hospitals and governments to make changes at the line of scrimmage to adapt to sudden changes. The equity markets are telling us that we will get through this, but it doesn’t feel great out there. We’ll elect a president in less than a month. We don’t know the escape velocity from the pandemic because it relies on unpredictable human behavior. “Omaha!”