- The Federal Reserve forecasts 6.5% GDP growth for 2021, compared to an average rate of about 2.3% for the 10 years of the last recovery.

- The current sentiment is that it is all to the good, but the bills related to massive Fiscal stimulus haven’t come due yet. Taxes will likely be higher.

- Now is an ideal time to consider advanced planning opportunities and timing of capital gains.

- While it is unclear if an inflation uptick will be transitory or more persistent, Equities have typically served investors well as an inflationary hedge.

- We believe that discipline and thoughtful consideration against long-term goals will be more important than ever.

After a sharp and sudden downturn starting in February 2020, the economy is poised for recovery. Pent up demand, massive fiscal stimulus and an accommodative Federal Reserve (the Fed) should deliver growth in 2021. As of March 17, the Fed forecasts 6.5% GDP growth for 2021, compared to an average rate of about 2.3% for the 10 years of the last recovery. The evidence is already there. Restaurant, hotel and flight bookings are increasing rapidly; consumer confidence is rising; housing prices are rising. It is easy to look at things and say it will be the same as it ever was. But there will be differences. The Federal Government has taken on debt to finance all the stimulus from last year and this year. In addition to the growing obligations, the Biden administration has ambitions to increase the role of Government in the economy beyond anything we have seen in recent history. The current sentiment is that it is all to the good, but the bills haven’t come due. Taxes will likely be higher. Inflation has emerged as a legitimate fear. Regulations have unknown consequences when established.

Whether the new public investments and higher inflation are good for the economy will be a story for posterity. As investors, we need to prepare for very different times, but we don’t foresee a whole new playbook.

Taxes generally are triggered by transactions. We believe limiting turnover and tax loss harvesting will remain good practices and will be even more important in a regime that may not provide as preferential treatment of capital gains as we have seen in recent history. We don’t know exactly how taxes will change, but we know that they will. For taxpayers likely to hit the highest rates, we recommend preparing for a lower maintenance portfolio. First, clean up major issues before the new rates arrive. Our sell priorities are: 1) concentrations greater than 10% of the portfolio, 2) companies with stretched valuations or execution issues, and 3) things that are getting in the way of progress. We recommend taking a second look at things you plan to do in the next few years with a greater sense of urgency. The wealth transfer tax laws may never be more favorable than they are currently and we anticipate certain advanced planning techniques will soon be challenged.

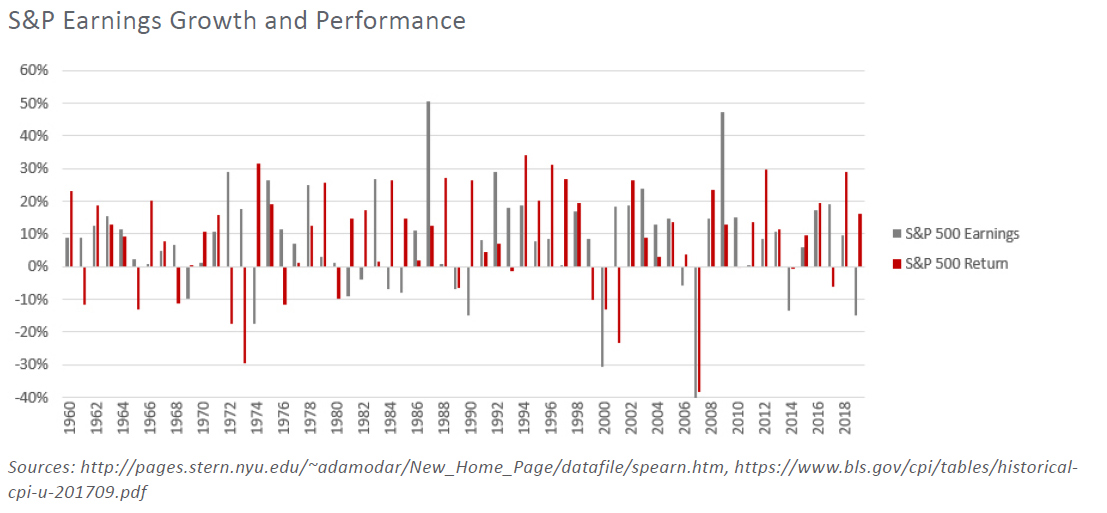

Inflation has the same compounding effect as interest. The real return is the difference between the absolute return and the rate of inflation. This is the increase in the spending power of your saved dollars. We believe that a long-term perspective is critical to driving a real return. A big single year return followed by years of underperformance will simply allow inflation to catch up. Stocks are an effective means of battling the deterioration in spending power caused by inflation; pricing power allows revenue growth at or above the rate of inflation; and companies can gain efficiency over time limiting the impact of inflation on costs. At the same time, inflation drives higher interest rates, which reduce the valuations of stocks all else equal. We could be looking at a period of lower returns, but equities do offer two benefits. First, they tend to grow with inflation. Second, during periods in which they don’t, they tend to catch up fast if an investor maintains the position. A long-term perspective is critical. Between 1960 and 2020, the S&P 500 delivered an annualized return of 7.2% while S&P 500 earnings increased 6.5% and inflation increased 3.7% over the same period. Between 1968 and 1982, a period characterized by very high rates of inflation, the S&P 500 returned 2.4% annualized while inflation increased at an average annual rate of 8.2%. Over the same time period, S&P 500 earnings increased 7%. As rates started to fall in 1982, equities recovered all the underperformance quickly. Earnings didn’t have to come back, valuations did. Being in and out of the market would have been a low-probability strategy for success. The persistence of S&P 500 earnings and the relatively tight association with equity prices over time are encouraging.

We don’t know whether we are in a period akin to 1968. There are as many differences as similarities. With bank deposits and bonds offering paltry returns, equities offer the best hope for delivering a return greater than the rate of inflation, whatever that rate turns out to be.

Equities have anticipated better economic times ahead. Large cap growth led through most of 2020 with small cap and value stocks beginning to outperform as visibility on the vaccine and the election became clearer. The S&P 500 currently trades at 22.7X next 12-month earnings versus the historical average of about 16X over the past 25 years. The forecast earnings serving as the denominator represents 27% growth. Expectations are high; however, the use of the word “bubble” seems inappropriate. Valuations are skewed in different places for different reasons because of the damage or benefit associated with Covid shutdowns. Information Technology is trading at a high multiple because of proven growth and unlike in prior episodes enjoy strong cash flow and profitability. Consumer discretionary and industrials are trading at a high multiple because earnings are suppressed.

Interest rates are an open question with a significant impact on equity valuation. We don’t know how much the Fed’s accommodation and secular factors such as international trade and aging population will mute upward pressure on interest rates from high growth and some additional inflation. Higher rates from growth are a good thing. Inflation is more complicated. On August 27, 2020, the Fed released its statement on “Longer-Run Goals and Monetary Policy Strategy” in response to a large-scale evaluation of the effectiveness of Fed policy. In effect, the statement seems to rebalance priorities with greater emphasis on a broader conception of full-employment and greater flexibility around the target inflation rate. Instead of targeting 2% inflation, the new strategy seeks to target an average of 2% inflation over time. The program is designed to fight the risk of deflation. European central banks also have been extremely accommodative. Inflation is expected to run higher through the earlier stages of the recovery as supply is constrained and demand is high. The million-dollar question is whether those near-term imbalances revert to the persistent trends of the prior 10 years. Most analysts believe that aging populations, enhanced price discovery (from the Internet) and a stable dollar are the primary drivers of tame inflation.

Low current rates and the potential for inflation are big concerns for bond investors. There likely isn’t any upside; however, we do still believe that investment grade bonds offer the most time-tested and cost- efficient means of managing total portfolio risk. After a long period of both stocks and bonds contributing to total performance, bonds will likely drag performance in the near future. That said, bonds are less volatile than stocks providing liquidity in volatile periods for stocks without having to sell depressed assets. Maintaining a portfolio with bonds no longer than 10 years until maturity and approximately even purchases at each maturity provides the flexibility of carrying bonds to maturity and reinvesting at prevailing rates at that time.

After a very difficult year, we are most likely looking at recovery but in many ways we are not returning to the same set of considerations of the past. The effectiveness of the vaccine, inflationary pressure and new tax and regulatory policy will develop as the year goes on. There will be many new considerations for investors. We believe that discipline and thoughtful consideration against long-term goals will be more important than ever.

After a sharp and sudden downturn starting in February 2020, the economy is poised for recovery. Pent up demand, massive fiscal stimulus and an accommodative Federal Reserve (the Fed) should deliver growth in 2021. As of March 17, the Fed forecasts 6.5% GDP growth for 2021, compared to an average rate of about 2.3% for the 10 years of the last recovery. The evidence is already there. Restaurant, hotel and flight bookings are increasing rapidly; consumer confidence is rising; housing prices are rising. It is easy to look at things and say it will be the same as it ever was. But there will be differences. The Federal Government has taken on debt to finance all the stimulus from last year and this year. In addition to the growing obligations, the Biden administration has ambitions to increase the role of Government in the economy beyond anything we have seen in recent history. The current sentiment is that it is all to the good, but the bills haven’t come due. Taxes will likely be higher. Inflation has emerged as a legitimate fear. Regulations have unknown consequences when established.

Whether the new public investments and higher inflation are good for the economy will be a story for posterity. As investors, we need to prepare for very different times, but we don’t foresee a whole new playbook.

Taxes generally are triggered by transactions. We believe limiting turnover and tax loss harvesting will remain good practices and will be even more important in a regime that may not provide as preferential treatment of capital gains as we have seen in recent history. We don’t know exactly how taxes will change, but we know that they will. For taxpayers likely to hit the highest rates, we recommend preparing for a lower maintenance portfolio. First, clean up major issues before the new rates arrive. Our sell priorities are: 1) concentrations greater than 10% of the portfolio, 2) companies with stretched valuations or execution issues, and 3) things that are getting in the way of progress. We recommend taking a second look at things you plan to do in the next few years with a greater sense of urgency. The wealth transfer tax laws may never be more favorable than they are currently and we anticipate certain advanced planning techniques will soon be challenged.

Inflation has the same compounding effect as interest. The real return is the difference between the absolute return and the rate of inflation. This is the increase in the spending power of your saved dollars. We believe that a long-term perspective is critical to driving a real return. A big single year return followed by years of underperformance will simply allow inflation to catch up. Stocks are an effective means of battling the deterioration in spending power caused by inflation; pricing power allows revenue growth at or above the rate of inflation; and companies can gain efficiency over time limiting the impact of inflation on costs. At the same time, inflation drives higher interest rates, which reduce the valuations of stocks all else equal. We could be looking at a period of lower returns, but equities do offer two benefits. First, they tend to grow with inflation. Second, during periods in which they don’t, they tend to catch up fast if an investor maintains the position. A long-term perspective is critical. Between 1960 and 2020, the S&P 500 delivered an annualized return of 7.2% while S&P 500 earnings increased 6.5% and inflation increased 3.7% over the same period. Between 1968 and 1982, a period characterized by very high rates of inflation, the S&P 500 returned 2.4% annualized while inflation increased at an average annual rate of 8.2%. Over the same time period, S&P 500 earnings increased 7%. As rates started to fall in 1982, equities recovered all the underperformance quickly. Earnings didn’t have to come back, valuations did. Being in and out of the market would have been a low-probability strategy for success. The persistence of S&P 500 earnings and the relatively tight association with equity prices over time are encouraging.

We don’t know whether we are in a period akin to 1968. There are as many differences as similarities. With bank deposits and bonds offering paltry returns, equities offer the best hope for delivering a return greater than the rate of inflation, whatever that rate turns out to be.

Equities have anticipated better economic times ahead. Large cap growth led through most of 2020 with small cap and value stocks beginning to outperform as visibility on the vaccine and the election became clearer. The S&P 500 currently trades at 22.7X next 12-month earnings versus the historical average of about 16X over the past 25 years. The forecast earnings serving as the denominator represents 27% growth. Expectations are high; however, the use of the word “bubble” seems inappropriate. Valuations are skewed in different places for different reasons because of the damage or benefit associated with Covid shutdowns. Information Technology is trading at a high multiple because of proven growth and unlike in prior episodes enjoy strong cash flow and profitability. Consumer discretionary and industrials are trading at a high multiple because earnings are suppressed.

Interest rates are an open question with a significant impact on equity valuation. We don’t know how much the Fed’s accommodation and secular factors such as international trade and aging population will mute upward pressure on interest rates from high growth and some additional inflation. Higher rates from growth are a good thing. Inflation is more complicated. On August 27, 2020, the Fed released its statement on “Longer-Run Goals and Monetary Policy Strategy” in response to a large-scale evaluation of the effectiveness of Fed policy. In effect, the statement seems to rebalance priorities with greater emphasis on a broader conception of full-employment and greater flexibility around the target inflation rate. Instead of targeting 2% inflation, the new strategy seeks to target an average of 2% inflation over time. The program is designed to fight the risk of deflation. European central banks also have been extremely accommodative. Inflation is expected to run higher through the earlier stages of the recovery as supply is constrained and demand is high. The million-dollar question is whether those near-term imbalances revert to the persistent trends of the prior 10 years. Most analysts believe that aging populations, enhanced price discovery (from the Internet) and a stable dollar are the primary drivers of tame inflation.

Low current rates and the potential for inflation are big concerns for bond investors. There likely isn’t any upside; however, we do still believe that investment grade bonds offer the most time-tested and cost- efficient means of managing total portfolio risk. After a long period of both stocks and bonds contributing to total performance, bonds will likely drag performance in the near future. That said, bonds are less volatile than stocks providing liquidity in volatile periods for stocks without having to sell depressed assets. Maintaining a portfolio with bonds no longer than 10 years until maturity and approximately even purchases at each maturity provides the flexibility of carrying bonds to maturity and reinvesting at prevailing rates at that time.

After a very difficult year, we are most likely looking at recovery but in many ways we are not returning to the same set of considerations of the past. The effectiveness of the vaccine, inflationary pressure and new tax and regulatory policy will develop as the year goes on. There will be many new considerations for investors. We believe that discipline and thoughtful consideration against long-term goals will be more important than ever.